- Home

- About Journals

-

Information for Authors/ReviewersEditorial Policies

Publication Fee

Publication Cycle - Process Flowchart

Online Manuscript Submission and Tracking System

Publishing Ethics and Rectitude

Authorship

Author Benefits

Reviewer Guidelines

Guest Editor Guidelines

Peer Review Workflow

Quick Track Option

Copyediting Services

Bentham Open Membership

Bentham Open Advisory Board

Archiving Policies

Fabricating and Stating False Information

Post Publication Discussions and Corrections

Editorial Management

Advertise With Us

Funding Agencies

Rate List

Kudos

General FAQs

Special Fee Waivers and Discounts

- Contact

- Help

- About Us

- Search

The Open Fuels & Energy Science Journal

(Discontinued)

ISSN: 1876-973X ― Volume 11, 2018

RMB Internationalization and Energy Prices: Evidence for Co-integration, Causality and Interaction Relationship

Fenghua Wen1, 2, Mi Deng2, Yuning Cai2, Cheng Peng3, Eimear Zhang1, Yong Tang1, *

Abstract

Objective:

Energy pricing in the international energy market is the key point for RMB internationalization, which can make the process further developed.

Aim:

Therefore it is of practical significance to study their co-integration relationship and causality, and though the impulse response to analyze their dynamic interaction relationship.

Method:

We take the Johansen co-integration and VAR model to explore the interaction between them.

Results:

Empirical results show that, firstly there is a long-term equilibrium between RMB internationalization and energy prices, and the change of short-term energy prices have a positive impact on the RMB internationalization index. Secondly, WTI oil price, domestic oil price and domestic coal price linearly Granger cause the RMB internationalization, but not vice versa. While RMB internationalization is only the Granger cause of the international coal price. Finally, the impulse response analysis shows that changes of energy prices play positive roles in promoting the internationalization of RMB.

Article Information

Identifiers and Pagination:

Year: 2017Volume: 10

First Page: 36

Last Page: 47

Publisher Id: TOEFJ-10-36

DOI: 10.2174/1876973X01710010036

Article History:

Received Date: 22/02/2017Revision Received Date: 07/03/2017

Acceptance Date: 19/05/2017

Electronic publication date: 25/07/2017

Collection year: 2017

open-access license: This is an open access article distributed under the terms of the Creative Commons Attribution 4.0 International Public License (CC-BY 4.0), a copy of which is available at: https://creativecommons.org/licenses/by/4.0/legalcode. This license permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

* Address correspondence to this author at the School of Business, Hunan City University, Yiyang, Hunan, China; Tel: 15874882888; E-mails: mailtowfh@126.com, dengmi0711@163.com

| Open Peer Review Details | |||

|---|---|---|---|

| Manuscript submitted on 22-02-2017 |

Original Manuscript | RMB Internationalization and Energy Prices: Evidence for Co-integration, Causality and Interaction Relationship | |

1. INTRODUCTION

A world or global currency is one that is transacted internationally, with no set borders. As the study of Helleiner, Kirshner [1Eric, H.; Kirshner, J. The future of the dollar; Cornell University Press, 2012. ], there are two key points for world currency, which are whether one can be reserve currency held by the central bank and open financial system that allows capital flow without restriction. For a long time, as the U.S. has the world’s largest economy, most international transactions continue to be conducted with the U.S. dollar. However, RMB became increasingly used as an international currency, and it has been qualified to internationalize for following reasons: China was the world second largest economy; RMB exchange rate was stable and we all have strong confidence; financial system reform makes China more open. According to Society for Worldwide Interbank Financial Tele communication [2SWIFT, Chinese Yuan demonstrates strong momentum to reach #4 as an international payments currency. 2015, 01-22.] data shows that the yuan has exceeded the Yen in August 2015, becoming the world's fourth largest payment currency, after the U.S. dollar, the euro, the pound. At the end of November, 2015, the RMB was designated as one of the world’s global currencies, IMF decided to include the Chinese yuan in its special drawing rights (SDR) basket of reserve currencies currently comprised of the U.S. dollar, euro, British pound and Japanese yen.

The RMB internationalization process has made some achievements, hence the internationalization of the RMB related research has become increasingly important. And the energy trade pricing and settlement binding power is the starting point for the rise of international commodities, such as the nineteenth Century coal Sterling system, as well as the twentieth Century Petro-dollar system, which shows that there is a close relationship between the currency internationalization and energy [3Wang, Y.; Guan, Q. The invoice currency of carbon trading: Theory, reality and choices. J. Contemp. Asia. Pac., 2009, 01, 110-128.]. The interaction between the RMB and the energy prices has also become a hot topic in the discussion of the academic study and social area [4Bal, D.P.; Rath, B.N. Nonlinear causality between crude oil price and exchange rate: A comparative study of China and India. Energy Econ., 2015, 51, 149-156., 5Liu, L.; Fang, Y.; Zhang, J. Dynamic correlations between international oil price and RMB Non-deliverable forwards returns. J. Int. Trade., 2014, 5(3), 224-235.]. In fact, in recent years, with the weakening relationship between the U.S. dollar and oil, and the non-dollarization of oil is becoming more and more apparent, energy valuation by the original single currency valuation may shift to a variety of common currency denominated [6Mileva, E.; Siegfried, N. Oil market structure, network effects and the choice of currency for oil invoicing., 2007., 7Lee, J.W. Will the renminbi emerge as an international reserve currency? World Econ., 2014, 37(1), 42-62.]. For now, the influence of the RMB internationalization is increasing year by year because of China's economic boost and political stability. Of course, the impact of the RMB to achieve the internationalization of the pound or the dollar is too early, but with the further development of China's economy and the government to actively promote the internationalization of the RMB, the yuan is likely to become one of the currency impacting the energy prices.

Energy invoicing currency is generally an international currency or a key currency. As energy currency represents a strong currency status, such as the oil market generally uses U.S. dollar for invoicing and settlement, the coal market mostly adopts the euro denominated [8Goldberg, L.S.; Tille, C. Vehicle currency use in international trade. J. Int. Econ., 2008, 76, 177-192.]. The dollar has maintained a very high position in the energy prices. The researches about whether the US dollar affects the oil price is still the hit now. Sadorsky [9Sadorsky, P. The empirical relationship between energy futures prices and exchange rates. Energy Econ., 2000, 22(2), 253-266.] uses co-integration method and Granger causality test to reveal the relationship between the energy futures price of crude oil and the U.S. trade weighted index, and found that the U.S. dollar exchange rate will impact on energy futures prices. Other scholars have similar conclusions, like Salimi and Yousefi [10Salamis, A.; Yousefi, A.A. Conformational changes and phase transformation mechanisms in PVDF solution cast films. J. Polym. Sci. Pol. Phys., 2004, 42, 3487-3495.], Lizardo and Mollick [11Lizardo, R.A.; Mollick, A.V. Oil price fluctuations and US dollar exchange rates. Energy Econ., 2010, 32(2), 399-408.] and Reboredo, Rivera-Castro and Zebende [12Reboredo, J.C.; Rivera-Castro, M.A.; Zebende, G.F. Oil and US dollar exchange rate dependence: A detrended cross-correlation approach. Energy Econ., 2014, 42, 132-139.]. Eichengreen, Chitu and Mehl [13Eichengreen, B.; Chitu, L.; Mehl, A. A. Network effects, homogeneous goods and international currency choice: new evidence on oil markets from an older era. working paper. 2014.] think that the pricing of oil will break through the dollar based pricing system, and move toward a variety of currencies, and will be implemented for a period of time. From Campanella [14Campanella, M. The internationalization of the renminbi and the rise of a multipolar currency system. J. Self-Gov. Manage. Econ., 2014, 2(3), 72-93.], the internationalization of the RMB have the potential to change the current currency system. RMB internationalization on behalf of Asian currency built a new pattern of multi-polar international monetary system. Yifan Yuan [15Yuan, Y. The development status, problems and countermeasures of China’s carbon financial market. Low. Carbon. Econ., 2016, 07(01), 62-69.] emphasizes we should seize the opportunity to blind the RMB and carbon emission, promoting the carbon trading in RMB for establishing a better carbon financial market. J Deng, J.Q. He [16Deng, J.; He, J.Q. An empirical analysis of the influence of international oil price’s fluctuations on the exchange rate of RMB. Adv. Mater. Struct. Mech. Engs, 2016, 141-144.

[http://dx.doi.org/10.1201/b19693-30] ] apply co-integration model to find out the influence of international oil price on RMB exchange rate, and the result shows that increasing oil price brings about RMB appreciation pressure.

The above researches show that the RMB internationalization has the possibility to affect energy pricing and energy prices, while there are also researches about that energy pricing and energy prices will affect the process of internationalization of the RMB. Currency as a medium of exchange for commodity pricing and as a measure of international trade in the use of international trade is an important part of the currency application [17Cohen, B.J. The Further of Sterling as an International Currency; Macmillan: London, 1971. -19Chinn, M.; Frankel, J.A. Will the euro eventually surpass the dollar as leading international reserve currency? in G7 Current account imbalances: sustainability and adjustment. Available from: http://www.nber.org/books/clar06-2 (Accessed May, 2007).]. Studies have indicated that actively promoting the valuation of the yuan in the energy market will open up a new way for the internationalization of RMB, which is conducive to the internationalization of the RMB. Chen and Qian [20Chen, Z.; Qian, L. Energy pricing and settlement currency choice and currency internationalization. Sata. Decis., 2012, 05, 151-154.] established a profit maximization model, and found a new currency internationalization path, that is, firstly become energy pricing and settlement currency, and then gradually become the international currency. Other scholars have also carried out the research on the energy path of RMB internationalization [21Li, J.; Zhang, L. The determinants of currency internationalization and its implications for the internationalization of RMB: Based on the perspective of the international reserve currency and the valuation currency of international bond. J. Theory., 2014, 12, 76-82.-23Xu, Q.Y.; He, F. Influence of RMB Cross-border Settlement on the Chinese Economy. China World Econ., 2016, 24(1), 104-122.]. All of the above studies show that energy pricing and energy trade can provide a new international path for the internationalization of RMB, and the process of RMB internationalization is affected by the energy prices.

In summary, the current researches on the internationalization of the RMB and the energy prices are mainly focused on theoretical research, there are few empirical studies on the relationship between the internationalization of the RMB and the energy prices. Well, the co-integration model and causality test are widely used to find the lead-and-lag price mechanism [24Zhang, Y.; Wei, Y. The crude oil market and the gold market: Evidence for co-integration, causality and price discovery. Res. Plcy., 2010, 35(3), 168-177.]. In this paper, from the empirical point of view, we use Granger causality test, JJ co-integration test and VAR method, to study the relationship between the two variables. Unlike previous studies which use RMB exchange rate, we choose the Standard Chartered Bank RMB World Index as proxy of RMB internationalization, and discuss how both international and domestic energy prices fluctuations to affect RMB internationalization, which provides a more broad vision to understand the relationship. Furthermore, it’s significant to conduct the process of RMB internationalization.

2. DATA AND METHODS

2.1. Variables and Data Sources

The data used in this study consists of monthly observations for the Standard Chartered Bank RMB World Index (RGI), oil prices and coal prices. The RGI is the first market index to track the development of the RMB, so we select the Standard Chartered Bank RMB world index to measure the process of internationalization of the RMB. In the same time, we select WTI spot price (WTIOIL) and Daqing crude oil spot price (DQOIL) as the measure of the international and domestic crude oil prices, and select Australia BJ-coal prices (BJCOAL) and Qinhuangdao Port coal (QHDCOAL) as a measure of international and domestic coal prices. RGI comes from the Standard Chartered Bank Research Center, while WTI crude oil spot price data are from the US Energy Information Administration, and the rest of the crude oil and the coal price data were derived from the flush data center. Data are available from December 2010, the sample span from December 2010 to March 2015, and each variable has 52 data.Xt is the variables at time t ,lnXt represents the log of variables at time t, R_Xt=100*(lnXt− lnXt-1) stands for RGI and the oil/coal price return at time t.

The descriptive statistics data analysis shows in Table 1. ADF test results show that the logarithm of the RMB internationalization sequence and energy prices series are non-stationary time series, first-order difference sequences were stable.

2.2. Methodology

2.2.1. VAR Model

In this paper, Auto Regressive Vector (VAR) model is established as a benchmark model. Based on the internationalization of the RMB and the energy prices, the two variables VAR model is as follows:

|

|

In the above formula, R_RGIt stands for the internationalization of the RMB, R_Xt are the energy variables, representing the yield of each energy sequence.

|

2.2.2. Johansen Co-integration Model

Co-integration test is to investigate the existence of long-run equilibrium relationship among variables. Based on the VAR model, we can obtain the following equation:

|

Then, considering different restriction, Johansen co-integration can be expressed as following,

|

Where, yt is dependent variable, xt are independent variables, t is the trend term, ρo is the intercept.

2.2.3. Error Correction Mechanism

Given VAR model the ECM would be calculated from the below equation:

|

Where ecmt-1 is the error correction vector, α estimates the speed at which an endogenous variable returns to equilibrium after any change in exogenous variables.

3. RESULTS AND DISCUSSIONS

3.1. Long-term Equilibrium Between RGI and the Energy Market

In this paper, we use the Johansen co-integration test proposed by Johansen and Juselius [25Johansen, S.; Juselius, K. Maximum likelihood estimation and inference on co-integration with applications to the demand for money. Oxf. Bull. Econ. Stat., 1990, 52(2), 169-210.] to test whether there is a long-term equilibrium relationship between RMB internationalization and energy prices. The test results are shown in the following Table 2.

The co-integration test results can be seen from Table 2, which indicate that both the variables and equations are significant at 1% level, and both residual series are stationary, hence we may say there exists a significant co-integration relationship between the RGI and energy price. Put it another way, they have long-term equilibrium interaction for each other.

3.2. Short-term Adjustment and Granger Causality test between RGI and the Energy Market

Besides the long-term equilibrium across the RGI and energy market, we further introduce the error correction model [26Engle, R.F.; Granger, C.W. Co-integration and error correction: representation, estimation, and testing. Econometrica, 1987, 55(2), 251-276.] to study the short-term interaction across the two variables.

First of all, in this paper, the optimum lag order of the ECM models are selected according to the principle of minimum AIC value. The result is shown in (Table 3).

We choose different lag order for our model respectively according to the above results

3.2.1. RMB Internationalization and Oil Prices

Firstly, we explore the relationship between RMB internationalization and oil prices, estimated results are shown as follows.

Results in Table 4 tell that from the short-term perspective, the interaction across the RGI and the international oil price appears strong in terms of their price change on the same day at 1% level. Specifically, when the RGI changes 1%,the WTIOIL price changes 0.195% to the same direction; whereas the WTIOIL price changes 1%, the RGI changes 0.125%, which seems much weaker than the shock of the RGI to the WTIOIL price. Additionally, it can be found that although the long-term equilibrium between the WTIOIL price and the RGI may significantly adjust the short-term changes of the RGI and the WTIOIL prices and cause that their short-term changes do not deviate from their long-term equilibrium path very far, the adjusting extent appears quite limited. According to the value of ecm term in Table 4, the adjusting extent to the RGI short-term change is -0.013%, while theWTIOIL price change is 0.003%.

Results in Table 5 show that when the RGI changes 1%, the DQOIL price changes 0.069% to the same direction; whereas the DQOIL price changes 1%, the RGI changes 0.132%, which seems much stronger than the shock of the RGI to the DQOIL price. According to the value of ECM term in Table 5, the adjusting extent to the RGI short-term change is -0.043%, while the DQOIL price change is -0.038%.

According to the Granger causality test in Table 6, the oil prices linearly Granger causes the RMB internationalization, but not vice versa. The main reason is that Chinese yuan is in process of internationalization, which can not break the traditional energy pricing system and impact much more on the oil prices. As we all know, the oil market is U.S. dollar dominated.

3.2.2. RMB Internationalization and Coal Prices

Results in Table 7 show that when the RGI changes 1%, the BJCOAL price changes 0.089% to the same direction; whereas the BJCOAL price changes 1%, the RGI changes 0.197%, which seems much stronger than the shock of the RGI to the DQOIL price. This result is coincident with the study of Derya Ezgi Kayalar, C. Coskun Kucukozmen [25Johansen, S.; Juselius, K. Maximum likelihood estimation and inference on co-integration with applications to the demand for money. Oxf. Bull. Econ. Stat., 1990, 52(2), 169-210.], they find emerging oil importer markets are less vulnerable to oil price fluctuations. According to the value of ECM term in Table 6, the adjusting extent to the RGI short-term change is -0.038%, while the BJCOAL price change is -0.049%.

Results in Table 8 show that from the short-term perspective, the interaction across the RGI and the domestic coal price appears strong in terms of their price change on the same day at 1% level. Specifically, when the RGI changes 1%, the QHDCOAL price changes 0.052% to the same direction; whereas the QHDCOAL price changes 1%, the RGI changes 0.075%, which seems much weaker than the shock of the RGI to the QHDCOAL price. Additionally, according to the value of ECM term in Table 8, the adjusting extent to the RGI short-term change is -0.034%, while the WTIOIL price change is -0.033%.

The results in Table 9 shows that, there are only unidirectional Granger causality relationship. Specifically, the RGI significantly linearly Granger causes the international coal price, but not vice versa. Meanwhile, the domestic coal price significantly linearly Granger causes the RGI, without reversed Granger causality.

Based on above analysis, we find the domestic oil price have a stronger effect on RMB internationalization, whereas the international coal price plays more important role. As we all know, the coal price has decreased sharply since 2012, and he coal market in China is in recession, leading more coal import from abroad. Well, the coal price is dependent on international coal price, not the domestic price. Crude oil market has been dominated by U.S. dollar for a long time, but studies show that relationship between U.S. dollar and oil price is weaker because other strong currencies, such as RMB. The stronger influence of domestic oil price on RGI would be attributed to efforts of oil market reform, which makes domestic oil price more efficient.

3.3. The VAR Model and Impulse Response Function Analysis

The interaction mechanism and influence degree of each variable are simulated and analyzed by using impulse response function.

3.3.1. RGI and Oil prices

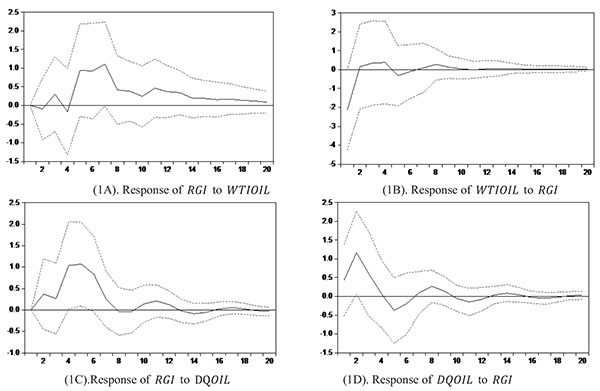

According to the previously established VAR model, the impulse response function is given as shown in Fig. (1 ).

).

|

Fig. (1) Responses to Cholesky one standard deviation innovations: RGI and crude oil price. |

Fig. (1A). represented that a unit of WTI crude oil price shocks, in the first two quarters, the RGI has a smaller negative response, then increased and reached the maximum positive response in the sixth to eighth quarters, then declining sharply around the 8th quarter, and finally remained in the positive response. In Fig. (1A). it is possible to observe that WTI price has a positive and durable effect on RGI . The rise in crude oil prices from the supply and demand level represents the increase in demand for crude oil, also shows that the economy is in a rising stage, the internationalization of the RMB with the economic upward trend of further development, the process is accelerated.

Fig. (1B). outlines the response of crude oil price to RGI. From the figure can be seen, in the short term the RGI has negative effects on crude oil prices. In spite of the positive response, the response is small and close to 0. We can see the internationalization of RMB developments bring short-term international oil prices fall, but a very short time to maintain. This is because China has failed to achieve the international crude oil invoicing, the degree of internationalization of the RMB is difficult to shake the market price of crude oil pricing.

Fig. (1C). discloses that the positive impact of the shock in the DQOIL to RGI is similar to the effect of WTIOIL, and reached a maximum impact in the 5th and 6th period, decreased around 10th quarter. Domestic crude oil price changes for the internationalization of RMB index has maintained a positive role, promotes the process of RMB internationalization. And the degree of influence is close to the international crude oil prices.

Fig. (1D). shows the positive and short term impact of RGI to DQOIL. In the second period reached the highest point, and then fall until the impact disappeared. It also shows that the internationalization of RMB for the impact of domestic crude oil price compared to the impact of international crude oil prices is more lasting.

From the above analysis, the oil price volatility has brought the RMB internationalization process quicken. In fact, in recent years, oil price fluctuation intensifies, and petrodollars system is being questioned. Studies have shown that petro dollars mean spillover effect has weakened in 2012, the dollar weakened the influence of crude oil price, the oil trade to de-dollarize tendency is more and more obvious. Since the global financial crisis, due to the weak U.S. and European economic growth, the impact of the RMB has been significantly improved, yuan has become the main reference currency in Asia. As a representative of the emerging countries, China's national strength has become increasingly strong, the yuan is also favored by investors. The yuan, which is gradually moving towards internationalization is more popular than the US dollar now. Sharp fluctuations in oil prices, the weakening of the status of the dollar, investors turned to the RMB market, which led to the internationalization process of the RMB. China take the initiative to seize the opportunity to further promote the process of internationalization of the RMB, the RMB internationalization achieved remarkable achievements. And the change of international and domestic oil prices for the extent of the impact of RGI approximation, is mainly because the domestic oil prices mainly affected by the impact of international oil prices, the impact of international oil prices on domestic oil prices significantly and long-term.

International oil prices and domestic oil prices in the short term has been affected by the RGI, and the response time of the domestic oil price is longer than the international oil price response time. Although the process of internationalization of the RMB has achieved remarkable achievements, but compared to the U.S. dollar and other international currencies, the RMB has little influence on oil pricing. For the domestic crude oil, along with the progress of the internationalization of the RMB, China's oil foreign trade settlement proportion in RMB clearing become bigger. That reduces the cost of oil imports, and domestic crude oil price volatility is exacerbated, then the response of crude oil shows a longer period of time to the impact of RGI.

3.3.2. RGI and Coal prices

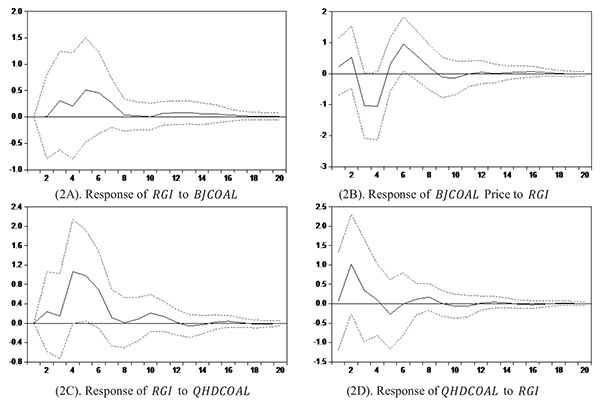

The results of RGI and coal price for the impulse responses are presented in Fig. (2 ).

).

|

Fig. (2) Responses to Cholesky one standard deviation innovations: RGI and COAL price. |

Fig. (2A). represented that a unit of BJ coal price shocks, the RGI has a positive response, and remained in the positive response for ten quarters. But the impact of international coal price change on RMB internationalization is obviously weaker than that of international crude oil price movements, and the impact of international oil on the internationalization of the RMB is more durable. This is mainly because, compared to the coal imports, China's import of oil quantity is huge, the international oil price for the internationalization of the RMB has a more significant effect.

Fig. (2B). outlines the impact of the RGI on the international coal prices have an obvious impact. International coal prices have a positive response in the first two periods. Then there is a large negative response, the biggest positive response occurs about 7th period, then gradually disappeared about 12th quarter. It can be seen that the internationalization of RMB to international coal prices has more significant influence, but the impact is not always maintained, and ultimately affect tends to 0, the internationalization of RMB for the impact of the international coal price also failed to produce long-term effects.

Fig. (2C). discloses that domestic coal price fluctuations for the RGI has a significant positive effect and in the 4th period reach the maximum. This is related to China's national conditions for China is not only a big country of coal consumption is also a major coal producing country.

Fig. (2D). shows coal prices showed a positive response for the RGI shock, and reached the highest in the second period, followed by a decline around the 12th period. The internationalization of RMB for domestic coal prices has a certain influence only in the short term. This is because China is a net importer of coal, and China does not have the right to control the coal pricing, the empirical results also show that the internationalization of RMB has no significant influence to the coal price.

From the above analysis can also see that both international coal prices and domestic coal prices for the RGI has positive effect to coal price fluctuation. Be similar with the reason for the oil market, the global financial crisis and the European debt crisis also brought fluctuations in coal prices, the dollar and currencies such as the euro decline in credit, investors look to the market of RMB, RMB trade settlement proportion increased, resulting in RGI rise, accelerating process of internationalization of the RMB. Domestic coal price on the impact of internationalization of the RMB is greater than the international coal price on the impact of the internationalization of the RMB, which is mainly because the carbon trading market unlike the oil supply is mainly dependent on OPEC. Coal supply shows diversified pattern, not only in developed countries and developing countries, thus makes the settlement currency of the carbon trading market is difficult to form a single currency. China itself is coal exporter, China in the carbon trading market have more initiative. Therefore, the influence of domestic coal price fluctuation on RMB internationalization index is greater than the international coal price fluctuation.

For improvement of national energy safety and process of RMB internationalization, an efficient mechanism should be established to control the shocks to RMB internationalization. Firstly, we should pay attention to energy prices fluctuations, avoiding sharp drastic changes of RMB exchange rate. Based on above impulse response function analysis, energy prices, whatever oil prices or coal prices, do have strong impact on RMB internationalization. We should take measures to accelerate the process of RMB internationalization by seizing the opportunity. Secondly, we need to focus on national energy safety. In Fig. (1), results show that both WTIOIL and DQOIL have similar impact on RGI, however the response of domestic oil price to RGI lasts longer than international oil price; in Fig. (2), we reveal that the influence of QHDCOAL on RGI is two times or so than BJCOAL. Therefore domestic energy markets are essentially put more concentration to encounter the RGI changes.

CONCLUSION

The analysis carried out in this paper reveals the interaction relationship between RMB internationalization and energy prices. We choose the Standard Chartered Bank RMB World Index to measure the process of internationalization of the RMB, select international / domestic oil and coal prices as a representative of the energy prices, using co-integration test, the Granger causality test, and the impulse response function analysis the degree of interaction between RMB internationalization and energy prices.

The empirical results show that the RMB internationalization and energy prices exist long-run equilibrium relationship and can be adjusted to the equilibrium state by Short-term adjustment. In addition to the international coal prices, international / domestic crude oil prices are the Granger cause of change in the RGI, and RGI is only the Granger cause of the international coal prices. From the impulse response function, we can see that crude oil price plays a positive role on the internationalization of RMB index process. Moreover, the internationalization of the RMB only produced a short-term impact for the price of crude oil, and the impact of domestic crude oil prices is much stronger than the international crude oil prices. For coal prices, coal prices have a positive impact on the internationalization of the RMB, and the impact of domestic coal prices on the internationalization of the RMB is stronger than the impact of international coal prices. For the impact of the internationalization of the RMB, the international coal prices in the short term are more volatile, while the domestic coal prices only exerts short-term response. Impulse response function diagram shows that the impact of energy price has a significant positive effect on the RMB internationalization index, which indicates that the energy prices volatility can promote the internationalization process of China's RMB. But the internationalization of the RMB for energy prices do not produce significant effect, indicating that the RMB in energy pricing system is still in the weak position. China still needs further efforts to impact on energy pricing.

There is obvious relationship between RMB internationalization and energy prices, especially energy prices fluctuations can significantly impact on RMB internationalization. Therefore, we should take measures to obtain the power of energy pricing in the process of RMB internationalization.

Firstly, a well-developed financial market would be helpful to RMB internationalization, undoubtedly, establishing energy commodity exchange is essential. The government should support these activities for influential energy market and make efforts to use RMB as settlement currency for energy trade. Dalian oil exchange has been set up and Huangpu oil exchange center is in arrangement. The establishment of energy exchange can contribute to energy prices marketization, and make sure that domestic energy price can be accepted widely.

Secondly, RMB is encouraged to use as payment currency when Chinese firms take in energy trade. As well-known, SDR inclusion grants the yuan international reserve currency status and provide some financial benefits. Meanwhile, RMB internationalization also gives Chinese companies rights to negotiating prices, helping them to reduce costs. We should use RMB as settlement currency and payment currency in international trade and commerce, promoting RMB internationalization for further step.

ETHICS APPROVAL AND CONSENT TO PARTICIPATE

Not applicable.

HUMAN AND ANIMAL RIGHTS

No Animals/Humans were used for studies that are base of this research.

CONSENT FOR PUBLICATION

Not applicable.

CONFLICT OF INTEREST

The authors confirm that this article content has no conflicts of interest

ACKNOWLEDGEMENTS

This paper was supported by National Social Science Foundation of China (No. 13CGL022), Scientific Research Fund of Hunan Provincial Education Department (No. 15A003, 15B046), Social Science Foundation of Hunan (Grant No. 15JD08), Hunan Provincial Natural Science Foundation (No. 16JJ1015).

REFERENCES

| [1] | Eric, H.; Kirshner, J. The future of the dollar; Cornell University Press, 2012. |

| [2] | SWIFT, Chinese Yuan demonstrates strong momentum to reach #4 as an international payments currency. 2015, 01-22. |

| [3] | Wang, Y.; Guan, Q. The invoice currency of carbon trading: Theory, reality and choices. J. Contemp. Asia. Pac., 2009, 01, 110-128. |

| [4] | Bal, D.P.; Rath, B.N. Nonlinear causality between crude oil price and exchange rate: A comparative study of China and India. Energy Econ., 2015, 51, 149-156. |

| [5] | Liu, L.; Fang, Y.; Zhang, J. Dynamic correlations between international oil price and RMB Non-deliverable forwards returns. J. Int. Trade., 2014, 5(3), 224-235. |

| [6] | Mileva, E.; Siegfried, N. Oil market structure, network effects and the choice of currency for oil invoicing., 2007. |

| [7] | Lee, J.W. Will the renminbi emerge as an international reserve currency? World Econ., 2014, 37(1), 42-62. |

| [8] | Goldberg, L.S.; Tille, C. Vehicle currency use in international trade. J. Int. Econ., 2008, 76, 177-192. |

| [9] | Sadorsky, P. The empirical relationship between energy futures prices and exchange rates. Energy Econ., 2000, 22(2), 253-266. |

| [10] | Salamis, A.; Yousefi, A.A. Conformational changes and phase transformation mechanisms in PVDF solution cast films. J. Polym. Sci. Pol. Phys., 2004, 42, 3487-3495. |

| [11] | Lizardo, R.A.; Mollick, A.V. Oil price fluctuations and US dollar exchange rates. Energy Econ., 2010, 32(2), 399-408. |

| [12] | Reboredo, J.C.; Rivera-Castro, M.A.; Zebende, G.F. Oil and US dollar exchange rate dependence: A detrended cross-correlation approach. Energy Econ., 2014, 42, 132-139. |

| [13] | Eichengreen, B.; Chitu, L.; Mehl, A. A. Network effects, homogeneous goods and international currency choice: new evidence on oil markets from an older era. working paper. 2014. |

| [14] | Campanella, M. The internationalization of the renminbi and the rise of a multipolar currency system. J. Self-Gov. Manage. Econ., 2014, 2(3), 72-93. |

| [15] | Yuan, Y. The development status, problems and countermeasures of China’s carbon financial market. Low. Carbon. Econ., 2016, 07(01), 62-69. |

| [16] | Deng, J.; He, J.Q. An empirical analysis of the influence of international oil price’s fluctuations on the exchange rate of RMB. Adv. Mater. Struct. Mech. Engs, 2016, 141-144. [http://dx.doi.org/10.1201/b19693-30] |

| [17] | Cohen, B.J. The Further of Sterling as an International Currency; Macmillan: London, 1971. |

| [18] | KENEN, The Role of the Dollar as an International Currency. Group of Thirty, Occasional Paper 1983, 13 |

| [19] | Chinn, M.; Frankel, J.A. Will the euro eventually surpass the dollar as leading international reserve currency? in G7 Current account imbalances: sustainability and adjustment. Available from: http://www.nber.org/books/clar06-2 (Accessed May, 2007). |

| [20] | Chen, Z.; Qian, L. Energy pricing and settlement currency choice and currency internationalization. Sata. Decis., 2012, 05, 151-154. |

| [21] | Li, J.; Zhang, L. The determinants of currency internationalization and its implications for the internationalization of RMB: Based on the perspective of the international reserve currency and the valuation currency of international bond. J. Theory., 2014, 12, 76-82. |

| [22] | Ma, J.; Xian, G. Development of international trade and the RMB internationalization. J. Nankai, 2014, 02, 136-141. |

| [23] | Xu, Q.Y.; He, F. Influence of RMB Cross-border Settlement on the Chinese Economy. China World Econ., 2016, 24(1), 104-122. |

| [24] | Zhang, Y.; Wei, Y. The crude oil market and the gold market: Evidence for co-integration, causality and price discovery. Res. Plcy., 2010, 35(3), 168-177. |

| [25] | Johansen, S.; Juselius, K. Maximum likelihood estimation and inference on co-integration with applications to the demand for money. Oxf. Bull. Econ. Stat., 1990, 52(2), 169-210. |

| [26] | Engle, R.F.; Granger, C.W. Co-integration and error correction: representation, estimation, and testing. Econometrica, 1987, 55(2), 251-276. |

| [27] | Kayalar, D.E.; Kucukozmen, C.C.A.; Kestel, S.S. The impact of crude oil prices on financial market indicators: Copula Approach. Energy. Econ, 2016, 61, 11-26. |